Damir Ćuća

October 14, 2021 • 7 minute read

Reviewed by Victor Leung

Fact Checked by The Basiq Team

Overview

Third party payment initiation in Australia is expected to go-live in mid 2022 via the New Payments Platform (NPP’s) PayTo. PayTo is an incredibly exciting development and will revolutionise the way consumers both pay and manage their payments. The Consumer Data Right (CDR) is also looking at payment initiation under its next policy iteration of ‘Action Initiation’.

On the 12th of October the NPP held a virtual event discussing the intersection of NPP’s ‘PayTo’ (formerly the Mandated Payment Service, MPS) and CDR’s Action Initiation. Basiq acknowledges the importance of both developments for third party payment initiation however presents three suggestions to encourage the benefit-sharing across both initiatives.

Finding 1: NPP’s PayTo will be the first brand of ‘Open Banking Payments’, however it is a closed ecosystem with mandates only accessible by those connected to the NPP

Description

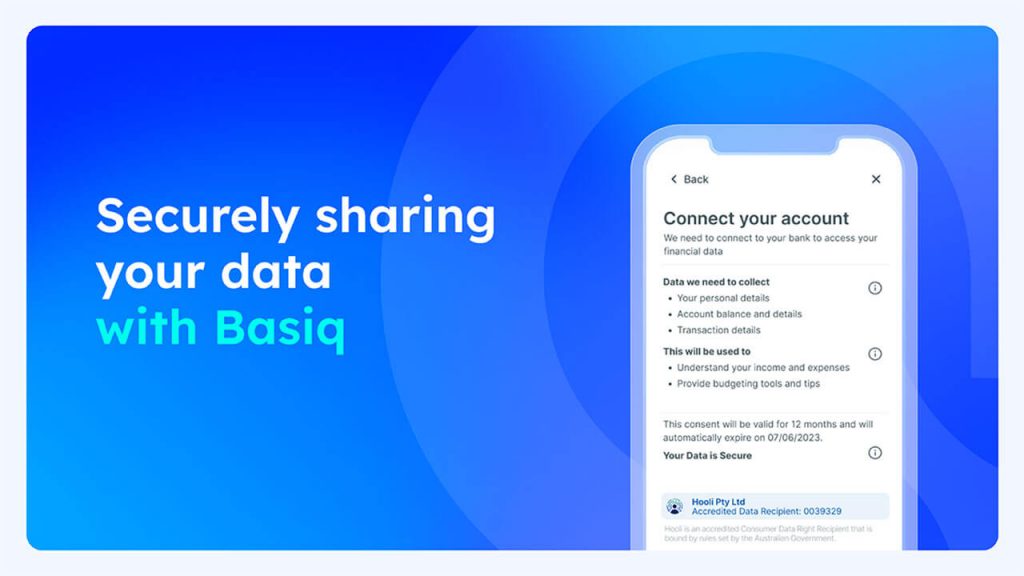

Mandates stored under NPP’s PayTo are stored in a centralised database. Each mandate is attached to a bank account (usually the PayID attached to that Bank account). Although a ‘single access point’ is desirable for those connected to the NPP, it reduces the open nature of data sharing that is distilled under the CDR.

A use case of this is an application where a consumer can see all their upcoming payment obligations in one spot, as well as assisting Banks with keeping track of where their PayTo obligations are held (currently, these sit at the merchant level, not the bank level).

The alternative to solve this is a federated digital identity framework however this is a significant piece of work and CDR is a more viable solution given its design as an Open Banking ecosystem.

Finding 2: There is a separation of consent flows between those outlined by CDR and those developed by the NPP.

Description

The NPP has its own consent flow that has been developed outside of the rigorous consent capture dictated by CDR. The capturing of a mandate will require a separate UX flow and require disclosure of different attributes to those at the CDR level. The session noted there will be workshops to integrate the consent flow however this should be prioritised so as to not affect the user experience and friction involved in the short term.

Suggestion

If there is a request to share data (say, logging into a microinvesting app and connecting your bank account) then there will be an additional step and consent flow to then authorise a recurring monthly top up of that account via PayTo. See flow below on consent for data-sharing and consent for a PayTo mandate:

Open app -> connect bank account -> consent to data sharing -> select auto-top up -> select PayTo -> consent to third party payment initiation -> complete

This adds an additional few steps to the user experience including confusion over a separation of the data that is shared, how long for, and how it is managed. Friction is brought into the user experience, where ideally the consent to capture data under CDR would include the consent to capture an NPP mandate, such that the flow would be as follows:

Open app -> connect bank account -> consent to data sharing and payment initiation -> complete

The above flow will be possible via Action Initiation, however it is encouraged that these consent flows merge in the short term.

Finding 3: PayTo alongside other Open Banking payments methods in the future (such as those via CDR’s action initiation) may confuse consumers

Description

If a consumer were to prefer to use an Open Banking direct debit payment – typified in the UK by the ‘Pay with Bank’ option, then there would be a separate UX flow (and payment button) for ‘Paying by Bank’ alongside PayTo.

This separation of experiences may be confusing for a customer, given that PayTo is ultimately a ‘Pay by Bank’ method, but using different payment rails. This will significantly hamper the uptake of both third-party payment initiation for consumers. Consumers are not fussed whether it goes via direct debit rails or NPP.

Suggestion

If PayTo were governed under the CDR framework, a consumer could ‘Pay by Bank’ and have the choice as to whether that is via PayTo or via Direct Debit, or even a one off payment via credit card – and the consent to capture would be as part of one flow, as mentioned in Finding 2. When CDR payment initiation arrives, merchants will also have to consider integrating multiple third party payment initiation rails.

Summary

Third party payment initiation in Australia will bring to life a number of exciting innovations, provide a slick user experience and utilise Australia’s world-leading fast payments infrastructure. There are some minor gaps between what is being achieved by PayTo and what CDR action initiation seeks to achieve. Basiq believes that alleviating these gaps will make for a great consumer experience and benefit all stakeholders involved in the future of third party payment initiation in Australia.

Article Sources

Basiq mandates its writers to leverage primary sources such as internal data, industry research, white papers, and government data for their content. They also consult with industry professionals for added insights. Rigorous research, review, and fact-checking processes are employed to uphold accuracy and ethical standards, while valuing reader engagement and adopting inclusive language. Continuous updates are made to reflect current financial technology trends. You can delve into the principles we adhere to for ensuring reliable, actionable content in our editorial policy.